An Overview of Assets: Part 2

What assets are right for me and how do I think about risk/reward?

Diversification is a common investing concept, one that may not be exciting yet is critically important, like many important disciplines. There are many levels to it. Beyond the concept of “not having all your eggs in one basket,” the real value comes from having uncorrelated returns between your assets. While it feels good when everything you own goes up at the same time, it feels equally bad, if not worse, when it’s happening on the way down. Emotions aside (and emotions are not an insignificant factor of investing), this concept is part of what distinguishes an amateur from a professional. A professional money manager is subject to career risk if their exposure is not carefully managed.

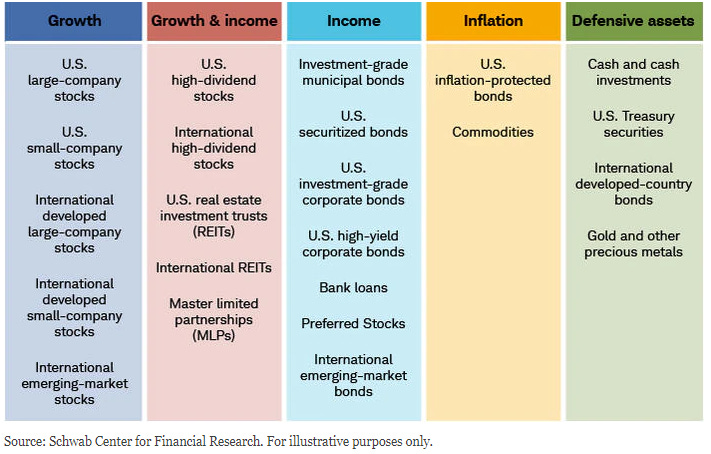

The question you to need to answer before “What is the right mix of assets?” is “What do you want the money to do?” That answer is different for every person based on age, retirement timeline, financial positioning, and risk tolerance. You could be young, but you could also be saving money for a down payment on a house. You could be older yet still be looking for growth-first. This infographic from Schwab provides a framework to think through what you seek from a given asset class.

Risk and Returns

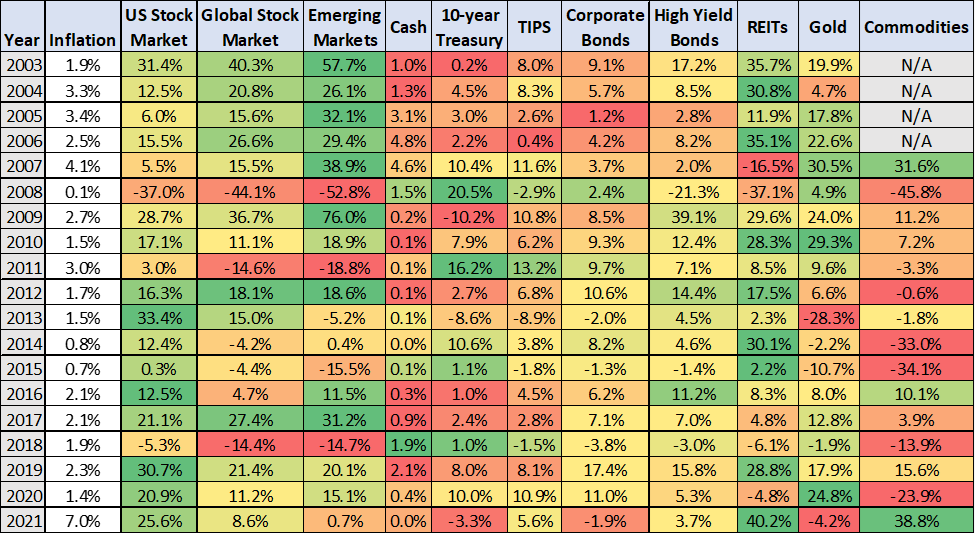

Here’s the data from some of the most popular asset classes since 2003. A useful takeaway is that returns by asset class vary each year, though market cycles can be identified. Look at Emerging Markets in the early 2000s or the remarkable bull run that the US Stock Market has seen the last decade. However, even looking at those 10 years for US Stocks, it was only the best performing asset (relative to this chart) in 3 of those years.

These statistics illuminate a couple other relevant takeaways:

The assets that produce the highest returns also produce the largest drawdowns

The most stable assets (looking at the standard deviation) tend to have lower returns

The last point to make here is that you can’t truly define a “best” asset class. It all depends on your personal and financial outlook. Frankly, there’s no reason to try. It’s like trying to identify the “best” food and eating only that all day, every day. You get different things from different foods. What’s the investing equivalent to a balanced diet? Read on…

Asset Allocation

Asset allocation is the process of spreading your money across various asset classes to create balance in your portfolio. It is part of how you manage risk. Well, ok, but what’s the easiest way to do that? Simply, an asset allocation fund. If you employ a financial advisor, chances are they have you in some form of asset allocation fund, as asset allocation is likely a significant part of what you are paying them to do. There are a few main types:

Target-Date Funds. These funds are targeted towards the time frame you expect to retire in. Over time, the mix of assets, and ensuing aggressiveness and conservativeness of the holdings, will shift accordingly. The exact year doesn’t matter as long as it’s close. All 401k plans have these funds (your 401k may be invested in one now), and it’s the simplest way to approach asset allocation.

Static Asset Allocation Funds. These funds have a pre-fixed % of funds allocated to each asset class. This ratio does not change. The 60/40 stocks to bonds is a classic example.

Dynamic Asset Allocation Funds. This is similar to a static fund except the fund manager has the freedom to change the allocation to various assets, within the strategy of the fund. For example, the prospectus of $FASGX indicates that they intend to maintain an overall asset mix of 70% stocks, 25% bonds, and 5% short-term cash / money market, but have the freedom to be within a range of 50-100% stocks, 0-50% bonds, and 0-50% short-tern cash / money market.

What Asset Allocation Looks Like

Let’s take a peek inside $SWYGX, a 2040 “Target-Date Fund.” I annotated the right margin and you can see there are 4 different types of assets, 8 counting asset sub-categories. You can imagine the complexity involved with doing this on your own. It’s something most people don’t have the time or interest in doing.

Weighting

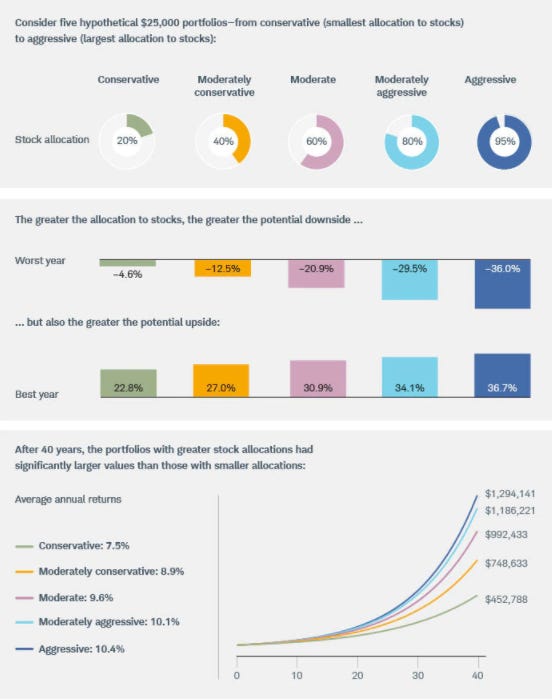

There’s no exact science, but I pay attention to how institutions design these funds. The primary adjustment you see is the weighting of equity. As you can see from the tables above, the only asset classes that have consistently produced double-digit returns over the last 20 years all fall into the stock/equity category. Looking at the 2040 Target-Date allocation above, you see a total 82% weighting towards stocks (adding up all the sub-classes). Schwab’s 2030 ($SWYEX) fund? 65%. The 2060 fund ($SWYNX)? 96%. Someone retiring in 38 years has plenty of time to weather a big drawdown in stocks. For the price of that risk, historical data shows they will generate the best returns. Someone retiring in the next decade or two should want more ballast in the portfolio and that’s what bonds can provide. Here’s one last visual from Schwab to put an exclamation point on it.

A Quick Notes On Fees

An important question to ask with any fund you own is, what’s the fee? $SWYGX above carries a reasonable .08%. Unlike what I see in target-date funds, many asset allocation funds have higher fees (.5%+). I would stay away from high fee funds at all costs. As investing has become democratized, there are plenty of low-cost options; no reason to let your money be siphoned away. This is easy to research through your brokerage. For example, Schwab has a “OneSource Select List” of funds with no sales load (a fee you pay off the top of money you invest; never pay this) or a transaction fee. Vanguard has many options too.

Additionally, what type of account you have matters. Most asset allocation funds are mutual funds, as opposed to ETF’s. ETF’s are more tax-friendly than mutual funds. This does not matter if you are in a retirement account like a 401k or a Roth IRA. However, it’s worth noting if you’re looking to asset allocate in a taxable account. A quick search yielded the below offerings from iShares. These are all large asset allocation ETF’s with low fees.

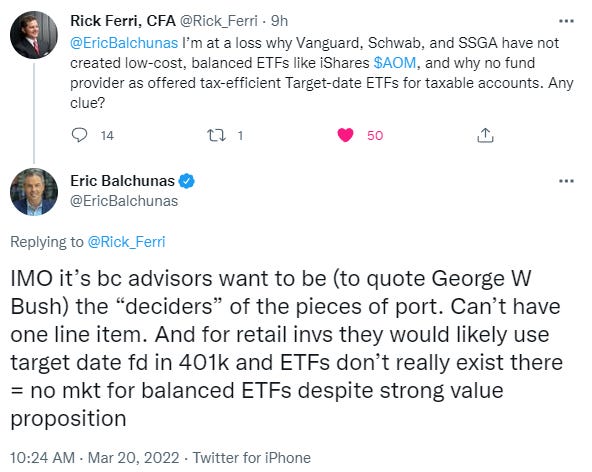

This morning I coincidentally stumbled across an intriguing Twitter take regarding why the aforementioned financial institutions don’t have offerings like iShares. The “can’t have one line item” reference below is an unfortunate byproduct of the sales element of the financial services industry. It would be easy to question the value proposition of paying an advisor to manage your money if it was all simply in one fund. That’s how you end up with “no market” for products like that as financial advisors are chief customers of places like Vanguard and Schwab. However, you can do it on your own…

What’s the bottom-line?

Have an asset allocation plan. Do the math on your own net worth. Include the equity in your house, and assess where there might be opportunity to diversify, whether into a new asset, or within a sub-category of an asset class you already own.

If you made it this far, thank you for reading!